Why your startup’s cash forecast breaks when you open a second entity

- Link copied

The cash forecast in your spreadsheet works fine until it stops. The breaking point is rarely a function of company size or revenue but the moment a second legal entity opens its first bank account.

The problem is not that finance teams suddenly become less capable. It is that the operating model changes faster than the tooling underneath it. Overnight, the CFO has abruptly moved from managing one balance sheet, one banking relationship, and one cash cycle, to global liquidity management across jurisdictions, currencies, and entities that were never designed to reconcile cleanly in a spreadsheet.

For most scaleups, that moment lands without much ceremony. You spin up an entity in Australia because a customer signed there. You open one in the UK to hire your first European employee. You set up a Singapore parent because the investors asked. Each step looks operational. The forecast model that has worked for two years suddenly has to do something different, and most of them cannot.

Spreadsheets survive longer than they should because they work exceptionally well in stable, single-entity environments. The problem is not the spreadsheet itself. The problem is that the business has evolved into something structurally different.

What changes when entity #2 opens

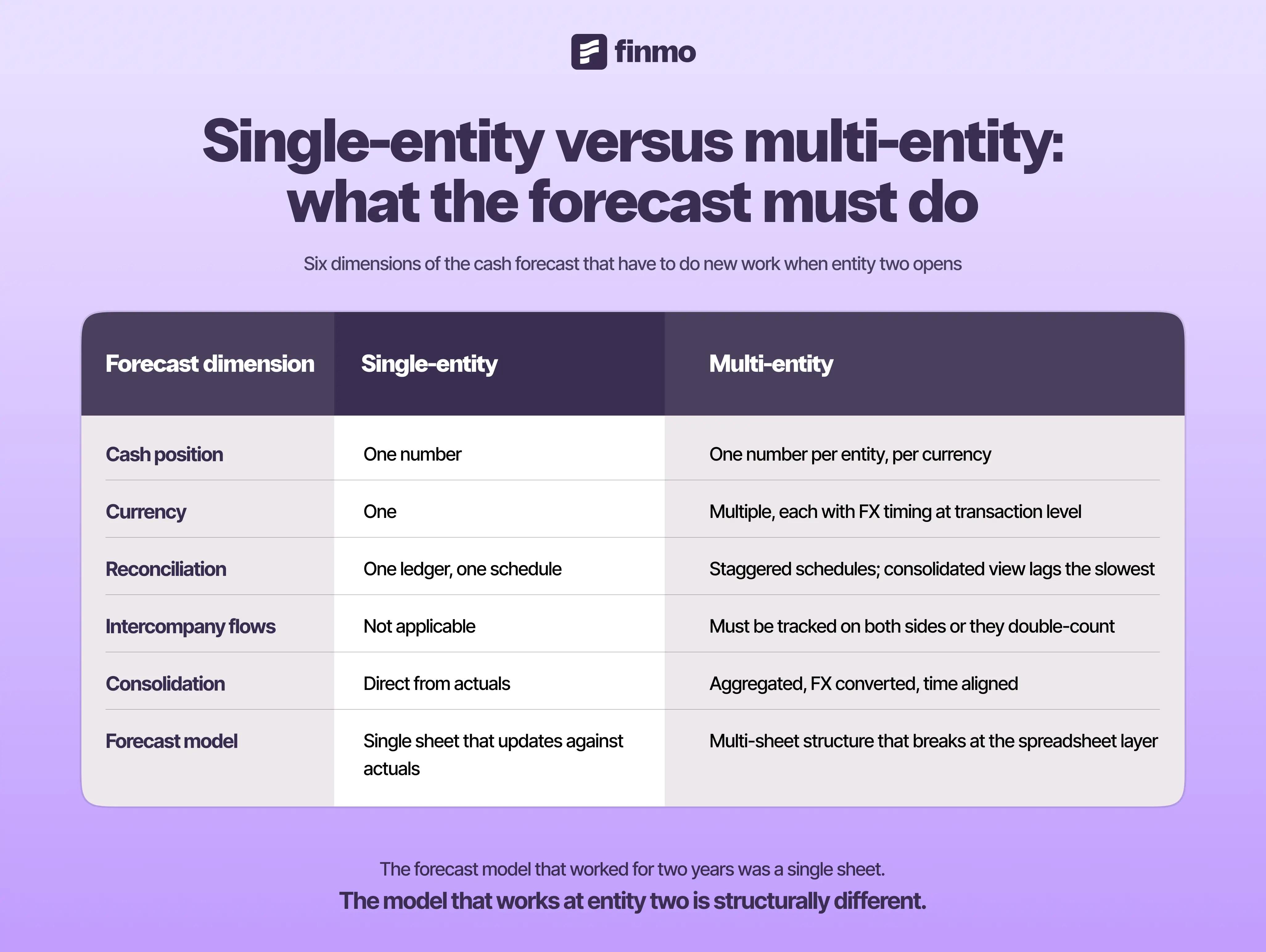

A single-entity cash forecast is a closed loop. Every dollar that comes in or goes out moves through one set of accounts. The starting balance, the inflows, the outflows, and the closing balance all reconcile to each other within one ledger. The forecast model can be a single sheet with rows for line items and columns for weeks. It can update against actuals because actuals only come from one place.

A multi-entity cash forecast is an open system. The inflows and outflows of each entity affect the inflows and outflows of the others through intercompany flows. Cash moves between entities to fund operations, settle invoices between sister companies, distribute profits, repay loans, and rebalance liquidity. The model now has to represent these internal movements as well as the external ones.

The structural change at entity two: a closed loop becomes an open system with intercompany flows

Four specific things break in the spreadsheet at this point.

Intercompany flows have to be modelled twice. Every cash movement between entity one and entity two appears as an outflow in one and an inflow in the other. The model either tracks both sides and reconciles them, or it tracks one side and double-counts at consolidation. Spreadsheet models almost always do the latter, because the discipline to reconcile both sides in a static model is more than most finance teams can sustain weekly.

Currency mix multiplies complexity. The Singapore entity might collect in SGD and USD. The Australian entity might collect in AUD and pay suppliers in USD. The UK entity might invoice in GBP, EUR, and USD. The forecast either consolidates to a single reporting currency at constantly changing rates, or it presents the position by currency with no consolidated view. Both approaches are imperfect. Both create FX exposure that the spreadsheet cannot quantify in real time.

Reconciliation timing fragments. Each entity reconciles to its own bank statements on its own schedule. The Australian books might close five days after the UK books. The Singapore parent might close another three days later. The consolidated forecast is only as fresh as the slowest closing entity, and the practical effect is that the consolidated view is always at least a week behind reality.

Audit and legal entity treatment diverge. Tax authorities, auditors, and regulators want each entity treated as a separate company. Operationally, the founder and the CFO want a consolidated view of cash across the group. The spreadsheet has to serve both purposes and usually serves neither well.

Each break compounds. When three land in the same quarter, the spreadsheet stops being useful.

The breaking point in the spreadsheet

There is a specific moment in the lifecycle of a scaleup spreadsheet model where the work to maintain it exceeds the value of the answer it produces.

It tends to land when the second currency moves from being a small share of activity to a material share. At ten percent of flow, the spreadsheet can ignore FX timing and use period averages. At forty percent of flow, the FX timing on each invoice and each payment matters, and the forecast that does not represent it is materially wrong.

It tends to land when the second entity reaches material trading volume. Below that point, the entity can be modelled as a cost centre with a single net cash impact. Above that point, it has its own working capital cycle, its own creditor and debtor positions, its own intercompany flows, and the spreadsheet has to represent all of them.

It tends to land when the board starts asking for a consolidated view that disaggregates by entity and by currency. The board wants to understand whether growth in one market is being funded by cash generated in another, whether FX exposure is concentrated in one corridor, whether the consolidated runway is fifteen months or eighteen months. The spreadsheet that gives one number cannot answer those questions. The spreadsheet that gives multiple numbers cannot reconcile them.

When all three land in the same quarter, the forecasting work consumes a full-time person and still produces a number the CFO does not fully trust.

What good looks like at this stage

The scaleups that scale through this point treat the cash forecast as a connected system. The shape of the answer is the same in every successful case.

Multi-bank cash visibility is the starting point: bank feeds connect directly from every account in every entity, with no manual export step. The starting balance for each forecast period is therefore live.

Intercompany flows are modelled once and surfaced on both sides automatically. The forecast cannot double-count or under-count because the system does the reconciliation.

Currencies are tracked by entity and consolidated to a single reporting currency at live rates. The CFO can see the position in any currency view they need without rebuilding the sheet.

The forecast updates against actuals as transactions clear, so the rolling thirteen-week view reflects what just happened rather than what was assumed two weeks ago.

Board reporting can be exported from the same source as the operational view, so the numbers in the board pack and the numbers in the forecast match by construction.

Every item on this list is operationally available today, at price points and implementation timelines that fit a Series A or Series B budget.

The longer you wait, the further you fall behind

The forecast that breaks at the second entity does not get easier at the third or the fourth. Each additional entity multiplies the complexity. The finance stack that got a scaleup from one entity to two is rarely the stack that gets it from 2 entities to 10.

The earlier finance teams recognise that treasury complexity scales non-linearly, the earlier they stop managing cash retrospectively and start operating it strategically.

We built Finmo for the moment finance teams transition from managing accounts to operating a global treasury layer. The platform connects banks, entities, currencies, payments, and forecasting into a single operational system, so scaleups can manage liquidity with the same visibility and control traditionally reserved for enterprise treasury teams.

FAQs

Why do cash forecasts break when you open a second entity?

A single-entity forecast is a closed loop, where all inflows and outflows reconcile within one ledger. A multi-entity forecast is an open system, where intercompany flows, currency mix, fragmented reconciliation timing, and audit and legal divergence all force the model to do work it was not designed for. The spreadsheet that worked for two years suddenly cannot represent the structure of the business.

What is a multi-entity cash forecast?

A multi-entity cash forecast represents the consolidated cash position across two or more legal entities, accounting for intercompany flows, currency mix, and the timing differences between when each entity closes its books. It is structurally different from a single-entity forecast: an open system with internal movements, not a closed loop with external flows only.

How do you forecast cash flow across multiple currencies?

The forecast either consolidates to a single reporting currency at live FX rates, or presents the position by currency with no consolidated view. The choice depends on what the board needs to see and how the entities operate. Either way, the model needs to handle FX timing at the transaction level, not at the period average, once currency mix is more than ten or fifteen percent of activity. Connected cash intelligence makes this tractable; spreadsheets do not.

When should you stop using spreadsheets for cash forecasting?

The trigger is rarely a single threshold. It tends to be the moment three things land in the same quarter: the second currency becomes a material share of activity, the second entity reaches material trading volume, and the board starts asking for a consolidated view that disaggregates by entity and by currency. Diagnostic signals show up earlier than most teams notice.

What's the difference between a TMS-Lite and an enterprise TMS for multi-entity forecasting?

An enterprise TMS is built for large organisations with full-time treasury teams, six-figure budgets, and twelve-month implementation timelines. A TMS-Lite delivers the operational capability for a scaleup: connected bank feeds, automatic intercompany reconciliation, multi-currency consolidation, and live forecasting at price points and implementation timelines that fit a Series A finance budget.

Jonathan Lew is CFO and COO of Finmo, a treasury management system with embedded payments built for companies operating across borders. Across corporate development at Nium during its scale into one of Southeast Asia's first fintech unicorns, investing at Jungle Ventures, and audit at EY, he has watched the same operational triggers break finance functions at every stage of growth. Finmo is licensed and regulated across 8 jurisdictions globally.