The founder's guide to cash visibility before you hire a CFO

- Link copied

Most founders I speak to can tell me their monthly burn rate within ten seconds. Ask them where their cash actually is right now, across every account, and the answer takes longer. Sometimes it takes a spreadsheet. Sometimes it takes logging into three bank portals.

That gap is what we call cash visibility, and most early-stage companies have very little of it.

The distance between knowing your burn and knowing your cash position is where founders lose time, miss signals, and make decisions on incomplete information. It is also the gap that a first finance hire is eventually brought in to close. The problem is that most startups wait until Series A or later to make that hire, and the symptoms of poor cash visibility sit unaddressed for a year or two before anyone owns them.

You do not need a CFO to close it. You need cash visibility.

What cash visibility actually means at your stage

Cash visibility is not a dashboard. It is not a report. It is the ability to answer three questions at any point during the week without opening a spreadsheet or logging into a bank portal. At its simplest, it is the treasury layer that sits between your bank accounts and your decisions:

- How much cash does the company have right now, across every account?

- How much of that cash is committed: payroll due, invoices approved, contracts signed but not yet billed?

- At the current rate, how many weeks of operating runway remain?

At pre-seed and seed stage, these questions feel simple. One bank account. One payroll. A handful of vendors. The founder can hold the answer in their head. The moment the company opens a second bank account, takes on a foreign-currency obligation, or signs a contract with payment terms longer than 30 days, the answer stops fitting in memory.

Most founders cross that threshold between twelve and twenty-four months after incorporation. The business is still too small for a finance hire, but the cash picture has grown past what any single person can track manually without a system.

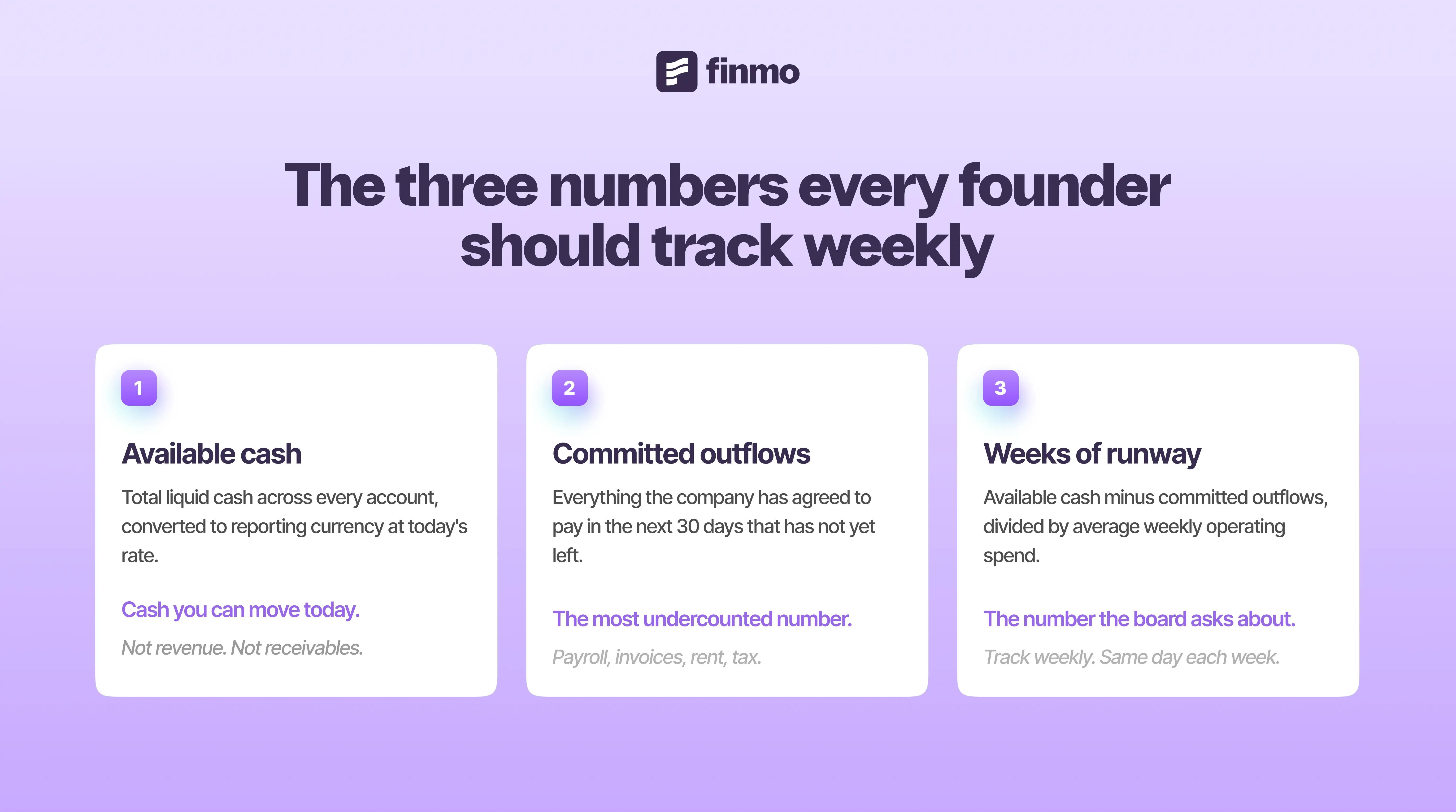

The three numbers every founder should know weekly

The founders who navigate this stage well tend to track three numbers on a fixed weekly cadence. Not monthly. Not when the board asks. Weekly, on the same day, before the week's decisions get made.

The three numbers that replace guesswork: available cash, committed outflows, and weeks of runway.

1. Available cash: The total liquid cash across every account the company holds, converted to your reporting currency at today's rate. Not revenue. Not receivables. Cash you can move today. If this number requires logging into more than one portal or updating more than one spreadsheet, the process is already more fragile than it should be.

2. Committed outflows for the next 30 days: Payroll, approved invoices, rent, software subscriptions, contractor payments, tax obligations. Anything the company has agreed to pay that has not yet left the account. This is the number that founders most often undercount, because commitments live in contracts, approval threads, and verbal agreements, not in the bank balance.

3. Weeks of runway at current burn: Available cash minus committed outflows, divided by average weekly operating spend. This is the number the board will ask about. It is also the number that determines whether the founder sleeps well on Sunday night. If it changes by more than two weeks from one measurement to the next without an obvious cause, something in the business has shifted that needs attention.

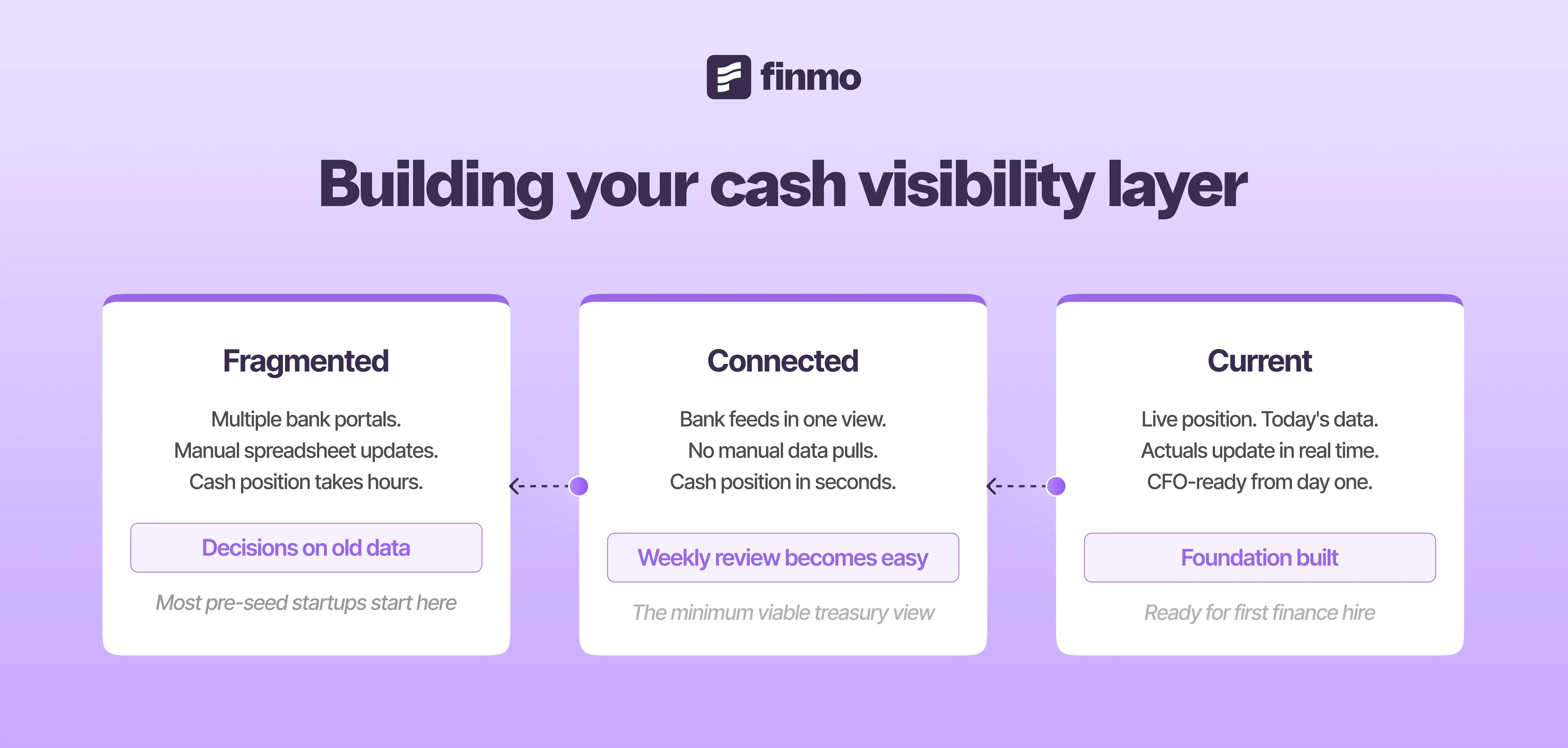

How to build a basic treasury view without a finance team

The infrastructure for tracking these three numbers does not need to be sophisticated. It needs to be consistent, connected, and current.

Connected means your bank accounts feed into one view. At pre-seed and seed, this might be a single bank with a single dashboard. The moment you open a second account, whether for FX, for a subsidiary, or because a payment provider holds a float, the view fragments. A live cash position that pulls from every account into one place is the single most valuable piece of financial infrastructure a founder can set up before hiring anyone.

Consistent means the numbers update on a fixed cadence without manual effort. The weekly review works only if the data is already there when the founder sits down. If updating the spreadsheet takes two hours before the review can happen, the review stops happening. The founders who sustain this discipline either automate the data pull or switch to a platform that connects directly to their banks.

Current means the numbers reflect today, not last Friday. A cash position that is five days old is a cash position that has already been overtaken by payments, receipts, and FX movements the founder cannot see. The further the data lags behind reality, the less useful the weekly review becomes, and the more the founder reverts to gut feeling and bank portal logins.

The progression from fragmented bank logins to a connected, current cash view.

What this does for your first finance hire

The founder who builds this view before hiring a CFO or finance lead does two things.

First, they make better decisions in the twelve to twenty-four months before that hire arrives. Every week, the three numbers surface the signals that matter: runway trending shorter, outflows spiking, cash concentrated in one account while obligations sit in another currency. The decisions that follow, whether to delay a hire, renegotiate payment terms, or move cash between accounts, are grounded in a live position rather than a remembered one.

Second, they hand the incoming finance hire a foundation that works. The new CFO or Head of Finance inherits connected bank feeds, a weekly tracking cadence, and a reporting baseline they can build on rather than build from scratch. The first 90 days go on strategic work rather than data archaeology.

Cash visibility is not a finance function responsibility. At the earliest stage of a company, it is a founder responsibility. The tools to do it well exist today, at price points that fit a pre-seed budget, with setup that takes days rather than quarters.

We built Finmo for this stage. The platform connects to your banks, surfaces your cash position across every account and currency, and gives you the weekly view that replaces spreadsheets and bank portal logins. You do not need a finance team to start.

You need visibility.

→ Read on Finmo Pulse: The new CFO playbook by David Hanna

FAQs

What is cash visibility for startups?

Cash visibility is the ability to see your total cash position across every bank account, in every currency, at any point during the week without manual data pulls. For startups, it means knowing your available cash, your committed outflows, and your remaining runway from a single connected view rather than from scattered bank portals and spreadsheets.

When should a founder start tracking cash position weekly?

From the moment the company opens a second bank account or takes on a foreign-currency obligation. Before that point, the founder can hold the cash picture in their head. After it, the picture fragments and decisions start relying on assumptions rather than data. Most startups cross this threshold between twelve and twenty-four months after incorporation.

What three numbers should founders track every week?

Available cash across all accounts (converted to reporting currency), committed outflows for the next 30 days (payroll, approved invoices, contracts), and weeks of runway at current burn. These three numbers surface the signals that matter for weekly decisions without requiring a full finance function to produce.

Do you need a CFO for cash visibility?

No. Cash visibility is a founder responsibility before the first finance hire. The infrastructure needed is a connected bank feed, a fixed weekly cadence, and data that reflects today rather than last week. The tools for this exist at price points that fit a pre-seed budget. A CFO builds on this foundation; they should not have to build it from scratch.

What is the difference between cash visibility and cash forecasting?

Cash visibility is knowing where your money is right now. Cash forecasting is projecting where it will be in the future. Visibility comes first. A forecast built on incomplete or stale cash data is unreliable. Founders should establish real-time cash visibility before investing in forecasting models.

David Hanna is CEO and Co-Founder of Finmo, a treasury management system with embedded payments built for companies operating across borders. With over 20 years in risk and compliance at PayPal, EY, ING, and Rapyd, he has seen how treasury complexity breaks businesses at every stage of growth. Finmo is licensed and regulated across 8 jurisdictions globally.