Our 13-week cash flow forecast cheatsheet for startup CFOs

- Link copied

Contrary to conventional wisdom, cash forecasting is not a reporting exercise. Today, it has become an operating discipline that helps finance leaders answer one question every week: how much cash will we have, and when will it arrive?

A 13-week cash flow forecast is the standard framework for answering that question at the right resolution. This cheatsheet, developed by myself and the Finmo senior leadership team, walks through how to build one – from setting up data feeds to running scenarios to connecting forecast outputs to treasury actions.

Why 13 weeks?

Thirteen weeks aligns with a financial quarter, giving you a rolling view of near-term liquidity while remaining close enough to influence decisions.

Monthly forecasts are too coarse – a payroll run, a delayed receivable, and a quarterly tax payment can all land in the same week and create a liquidity gap that a monthly view would miss. Daily forecasts generate noise. Payment timing varies by a day or two, and constant re-forecasting becomes a data assembly exercise rather than a decision-making tool.

Weekly resolution hits the practical middle ground. You capture payment timing patterns, catch short-term liquidity risks before they become emergencies, and maintain enough forward visibility to make decisions around hiring, expansion, fundraising, and major expenditures.

Step 1 – Start with live data

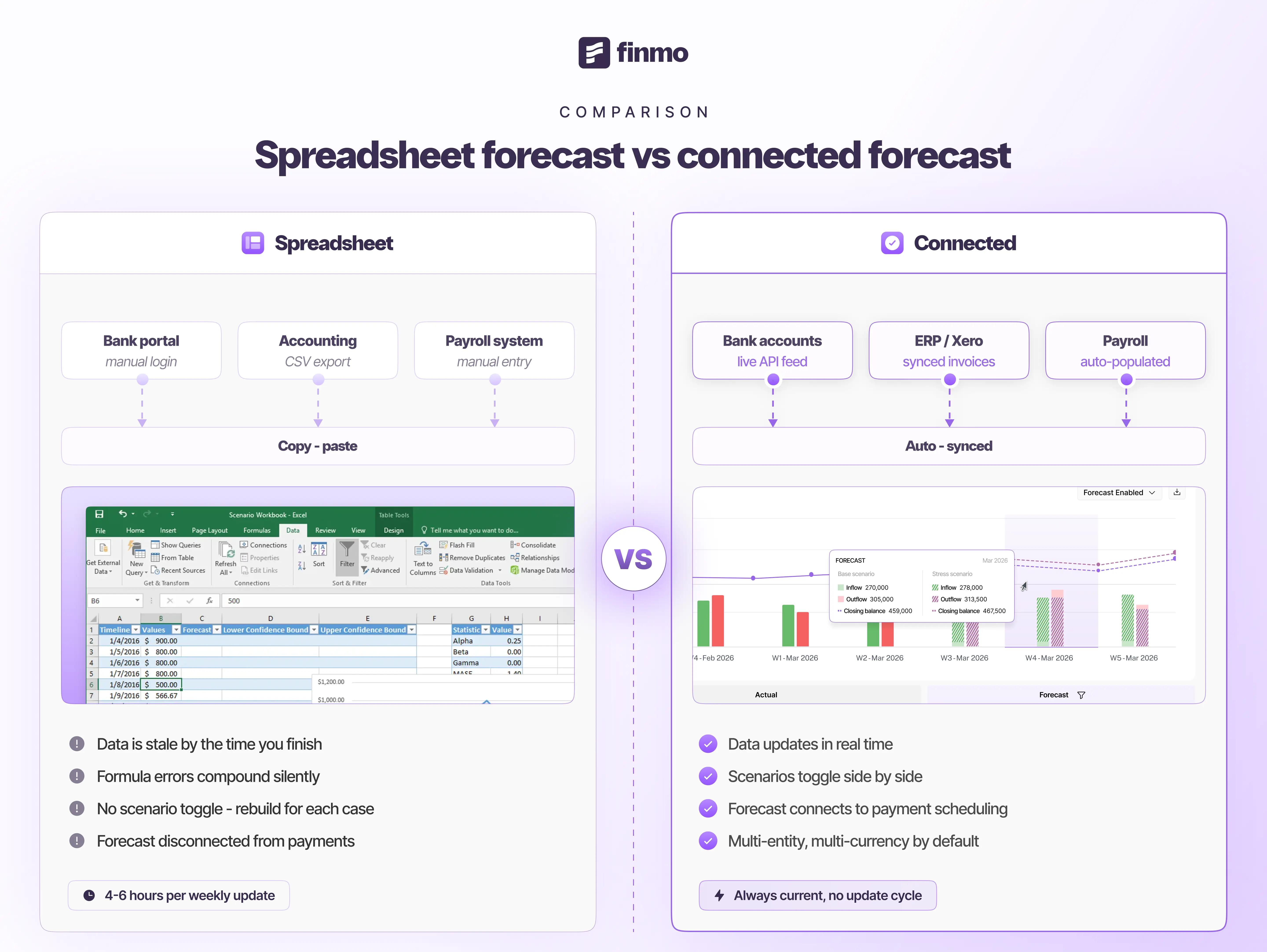

The accuracy of a forecast depends on the accuracy of its starting position. If your opening cash balance is 48 hours old because someone pulled bank data on Monday for a Wednesday meeting, every subsequent week in the model is off by whatever moved in those two days.

This is where spreadsheet forecasts break down first. The data assembly step – logging into bank portals, exporting CSVs from accounting systems, copying payroll figures from a separate platform – takes long enough that the numbers are stale by the time the forecast is built. Moving away from spreadsheets removes that lag entirely.

A connected forecasting platform automatically pulls balances, receivables, and payables from your financial systems, reducing manual work and ensuring forecasts start from current data rather than yesterday's assumptions.

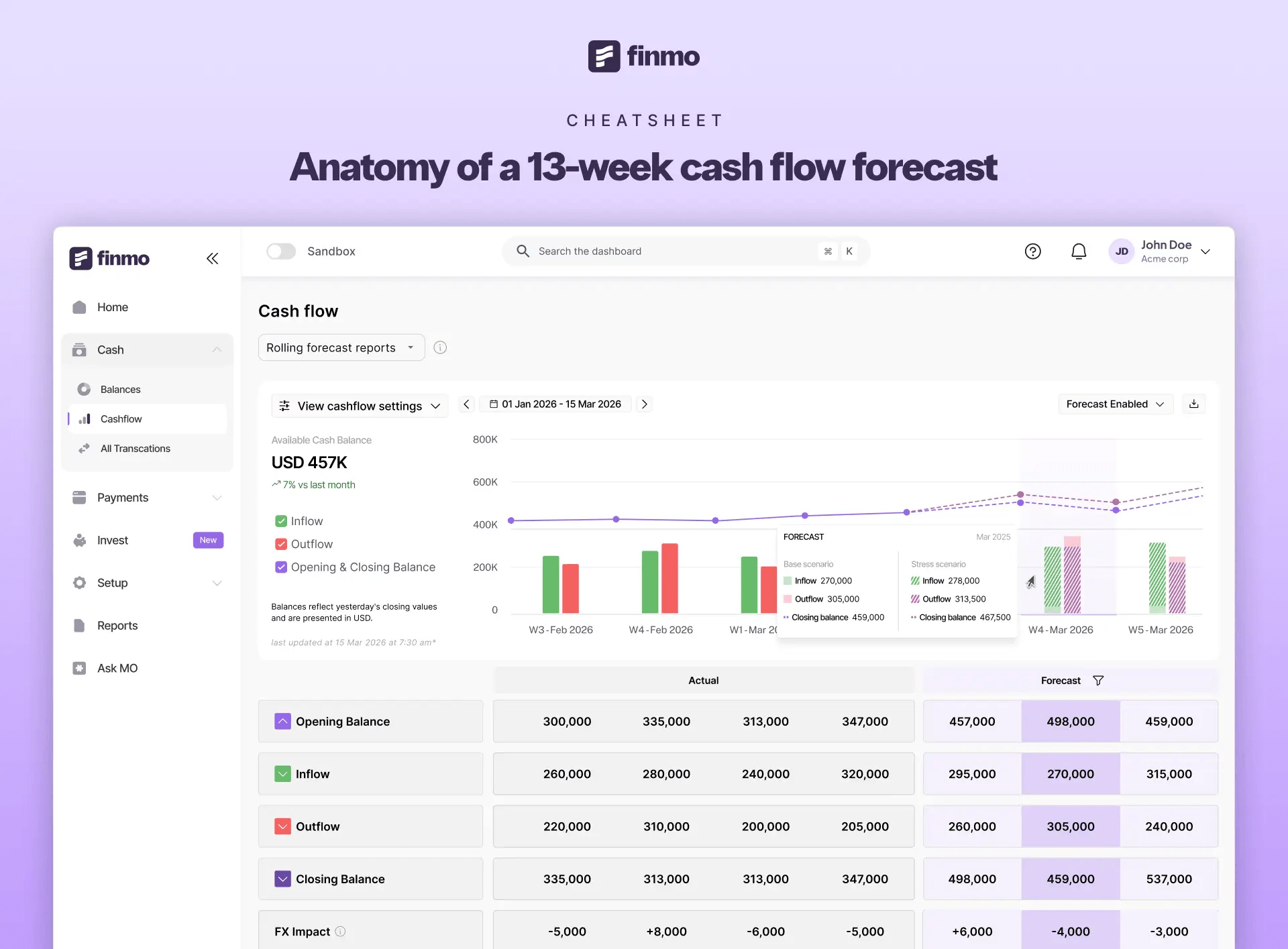

Finmo’s connected financial dashboard consolidates accounts across entities, banks, and currencies into a single source of truth for your global cash position. The forecast always starts from the current position.

Step 2 – Build your rolling window

A 13-week forecast is a rolling view. Each week, the earliest week drops off and a new Week 13 appears at the far end. You are always looking exactly one quarter ahead.

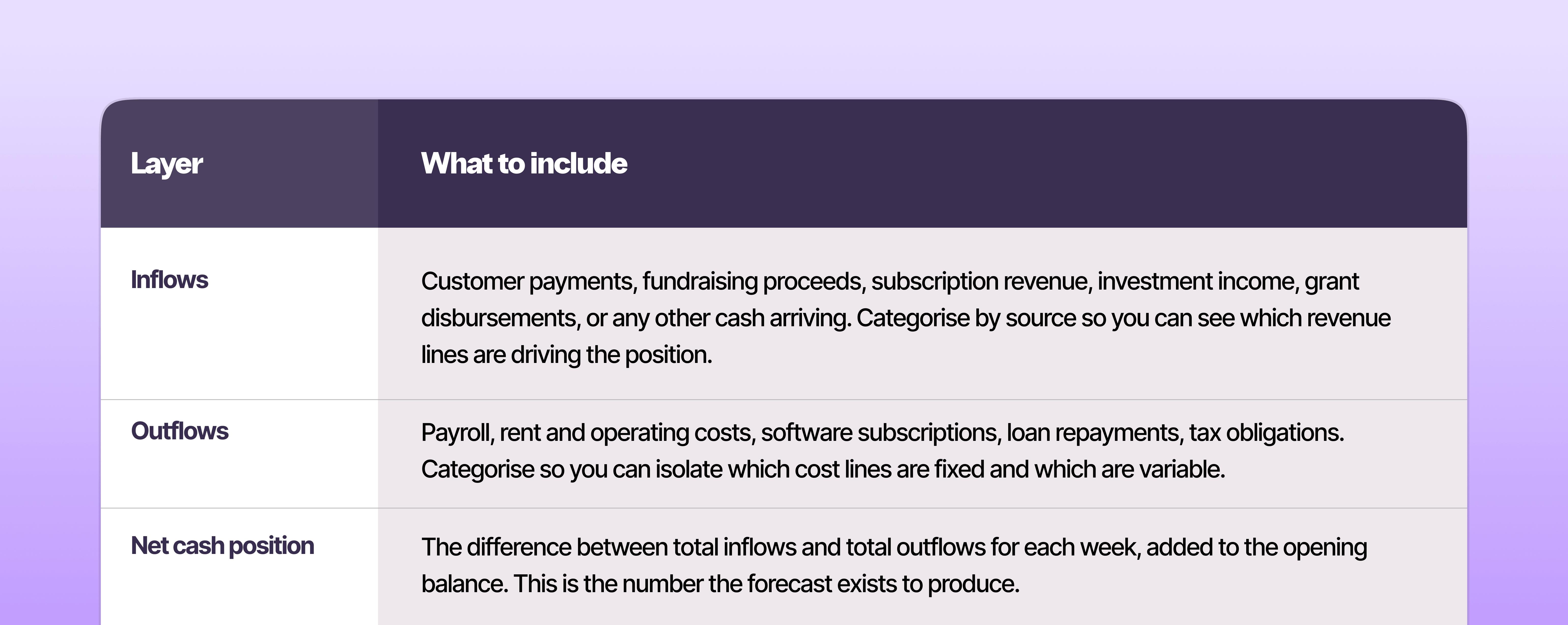

Structure the forecast around three layers:

With Finmo, inflows and outflows are continuously updated using live transaction data and historical payment behaviour, helping the forecast remain current without manual maintenance.

A 13-week forecast structures inflows, outflows, and net cash position across a rolling quarterly window with weekly resolution.

Step 3 – Layer in scenarios

A single forecast line tells you what is likely. Scenarios tell you what happens if something shifts.

Start with two: a base case and a stress case. The base case uses your best estimate of inflows and outflows, drawing on historical patterns. The stress case tests the variables most likely to move: delayed receivables (what if your largest customer pays 14 days late?), accelerated costs (what if you need to hire a month earlier than planned?), or an unplanned expense (a compliance cost, a hardware replacement, a contract termination).

The question each scenario should answer is concrete: how many weeks of runway do we have in the stress case? At what point does the cash position breach our minimum threshold? These answers inform real decisions – whether to draw on a credit facility, accelerate collections, or defer a non-critical hire.

Finmo’s scenario testing lets you toggle between base, stress, and custom scenarios side by side. You adjust assumptions in one view without rebuilding the model.

Step 4 – Connect forecast to action

A forecast is only as useful as the actions it triggers. The most common failure mode in cash forecasting is producing the report and filing it. A good forecast should change what you do next week.

If the forecast shows a gap in Week 8, the response depends on the size and cause: pull forward an invoice? Delay a supplier payment by five days? Restructure a payment schedule? These are treasury operations, and they should sit alongside the forecast.

Finmo connects forecasting to payments and AR/AP automation in one platform. When a scenario flags a cash shortfall, you can act on it in the same system – schedule a payment, follow up on a receivable, or restructure a payment run.

A connected forecast eliminates the data assembly step and links scenarios directly to treasury actions.

What changes when your forecast is connected

When the data assembly step disappears, the forecast becomes a live tool you check on demand. Finance teams that move away from spreadsheet-based cash management spend their time on analysis and decision-making rather than data gathering. The forecast updates itself. The scenarios re-calculate. The only manual step is deciding what to do with the information.

For startups operating with lean finance teams, this shift is significant. Time previously spent gathering data can be redirected toward planning, analysis, and strategic decision-making.

Explore how connected forecasting works inside Finmo.

FAQs

How often should I update a 13-week forecast?

Weekly. The model rolls forward each week automatically in a connected platform. If you are building manually, set a fixed day (typically Monday or Friday) and commit to the weekly refresh. Consistency matters more than precision.

What is the difference between a 13-week forecast and a monthly forecast?

Resolution and purpose. A monthly forecast gives a broad view across quarters or the full year. A 13-week forecast operates at weekly resolution, catching short-term liquidity risks (a payroll run coinciding with a delayed receivable, for instance) that monthly models miss. Most finance teams run both.

Can I build an accurate 13-week forecast in a spreadsheet?

You can build one. Keeping it accurate is the challenge. The data assembly step (bank exports, accounting CSVs, manual payroll entry) introduces staleness, and formula errors compound across 13 columns without visibility. A connected platform removes both problems by pulling live data and maintaining the rolling window automatically.

What should I do if the forecast shows a cash shortfall?

Identify the week and the cause. Then act: accelerate receivables collection, restructure payment schedules, delay discretionary spending, or arrange a short-term credit facility. The earlier the forecast surfaces the gap, the more options you have. This is why weekly resolution matters – a monthly forecast might not surface the shortfall until the window to respond has closed.

Jonathan Lew is Chief Financial Officer and Chief Operating Officer of Finmo, a treasury management system with embedded payments built for companies operating across borders. Finmo is licensed and regulated across 8 jurisdictions globally.