Finmo vs payment-first platforms: Why scaling finance teams need more than payment rails

- Direct answer

- What payment-first platforms were designed to do (and what they weren't)

- What treasury teams actually need beyond payments

- Why Finmo is a Treasury Operating System, not a payment platform with treasury features

- Side-by-side: Payment platforms vs Finmo (Treasury Operating System)

- When to use a payment platform vs when you've outgrown it

- Why Finmo is more than just a payment provider

- FAQ

- Link copied

Direct answer

Most fast growing global businesses assume a payment provider is enough to run their finance function. But that assumption only holds true until it doesn't.

Payment-first platforms move money cross-border, but they can't manage your treasury function. As operations expand across entities, banks, and currencies, scaling global businesses need cash visibility across every account, live forecasting, FX exposure management, and operational controls. None of these capabilities come built into spreadsheets or payment providers. Finmo is a Treasury Operating System (TOS) that unifies all of it in one layer.

In this guide, we discuss:

- What payment platforms were built for

- What treasury teams actually need

- Why Finmo is a TOS, not a payment tool

- Side-by-side comparison of payment platforms vs Finmo

- Self-diagnostic to identify your category

What payment-first platforms were designed to do (and what they weren't)

Payment-first platforms are B2B payment providers built for cross-border money movement. They solve a specific, important problem: getting money from A to B across currencies–quickly and at a reasonable cost. But there are also some scope limitations to these payment-first platforms.

Built for cross-border payment speed and cost

Most payment-first platforms have a clear set of capabilities, such as multi-currency accounts to receive and hold funds, competitive FX rates, international transfers, corporate cards, bill pay and AP automation, and payment links or invoicing support. For a team whose primary finance workflow is sending and receiving money internationally, the design fits the job, but that’s really where the scope ends.

Not built for enterprise treasury visibility

You cannot connect the bank accounts you already hold to payment platforms. That means, to use the multi-currency features these platforms advertise, you have to open and fund entirely new accounts with the provider itself. You would have to move cash off your existing banking relationships and onto the platform, just to gain access to its core functionality. Anything you leave in your existing banks, which is usually the majority of your cash, stays completely outside the platform's view.

In practice, this leads to your finance team running two parallel systems. One inside the payment platform, where you can see real-time activity for the funds held there, and another outside it, where the rest of your cash lives across multiple banks, currencies, and entities, tracked manually in spreadsheets, accounting tools, or weekly export routines. The platform was never designed to consolidate the two, which is why visibility breaks down the moment your business banks anywhere other than the platform itself.

Multi-currency accounts ≠ cash visibility

A multi-currency account is a single account that can hold and transact in several currencies at once. It is a useful feature for finance teams that need to receive and hold funds in multiple currencies so that they can make subsequent payments without needing to convert funds back and forth each time. Payment platforms have built this capability well.

But cash visibility is something different. It means knowing your complete cash position across every account, every entity, and every currency your business operates in. A multi-currency account shows you one slice of your cash, which is the slice that happens to live on the platform. Cash visibility shows you all of it, no matter where it sits.

What treasury teams actually need beyond payments

The job of a scaling finance team is to manage cash, end to end. Payments are only one workflow inside that broader responsibility. As the business grows, the other workflows multiply in volume and complexity, and each one needs capabilities that a payment-first platform was never designed to deliver.

Real-time cash position across all accounts

It can include every operating account, reserve account, and multi-currency wallet that are refreshed continuously and consolidated by entity and currency.

This single view is the foundation that the rest of your treasury function sits on. Without it, your forecasts end up being built on data that is already days old, and every question from the board about cash on hand requires a manual pull from different banks, platforms, and accounting tools. The faster your business grows, the more painful that manual work becomes.

Forward-looking cash forecasting

Backward-looking balances tell you where you are. A forecast tells you where you are going to be. For a scaling business, the second question matters more than the first, because every decision about hiring, expansion, fundraising, or working capital depends on what your cash position will look like three months from now. If your forecast lags behind by two weeks, it is no longer a forecast. It is just a record of what already happened.

FX exposure management at the entity level

A global business that earns in one currency and spends in others is exposed to currency movement every day. And CFOs needs to be able to answer questions like:

- How much cash is currently held in non-functional currencies and what is the exposure forecast by currency?

- What happens to the runway if the dollar moves five percent against the main operating currency?

- Should I hedge FX risk and at what effective hedge ratio?

Payment platforms can only optimise the cost of a single transaction. But treasury work optimises the position your business holds across every currency at once.

Working capital optimisation, not just payment execution

Working capital optimisation means making every dollar on your balance sheet do something useful. Some of that cash moves through the business as payments to suppliers, payroll, and tax. The rest sits in operating and reserve accounts, often making up the majority of your balance sheet at any given time.

A CFO running a treasury function should be able to do two things at once:

- Maintain controls, approvals, and reconciliation across every payment and every account, no matter which provider it runs through.

- Put surplus balances to work through integrated yield options, so the cash you are holding for next quarter's payroll or your next round of expansion is earning a return in the meantime.

Payment-first platforms do neither of these well.

Why Finmo is a Treasury Operating System, not a payment platform with treasury features

Finmo is a Treasury Operating System built to manage your entire cash function, with payments as one of the many capabilities inside it. Payment-first platforms are built the other way around, with payments at the centre and everything else bolted on later.

The core principle is complete cash visibility. Everything else is built on top of that foundation.

With Finmo, you can:

- Connect your existing bank accounts across entities and currencies, so every balance is visible in one place

- Open local currency accounts when you need them. You can hold and transact in 36+ currencies directly through Finmo, alongside your existing banking relationships

That principle plays out across all the areas of architecture and design that set a Treasury OS apart from a payment-first platform. Here is how each one works.

How the architecture is built: Treasury at the core, payments embedded

Treasury is the main focus with Finmo. It includes cash visibility, forecasting, FX exposure, and controls. Payments are just one of the many features of Finmo’s treasury operating system, alongside everything else.

How accounts are connected: your banks and Finmo in one view

You can connect the bank accounts you already hold across entities and currencies to your Finmo account, and you can even open multi-currency accounts in 36+ currencies whenever you need them.

Both types of accounts sit in the same view, in the same system. There is no closed ecosystem and no forced choice between using your bank or using the platform–they are part of the same operating layer.

How payment data is used: every transaction informs treasury decisions

Every payment your business makes includes data points about cash position, exposure, and timing. In a Treasury OS like Finmo, all that data feeds the forecast, updates the exposure view, and helps your finance team make the next treasury decision.

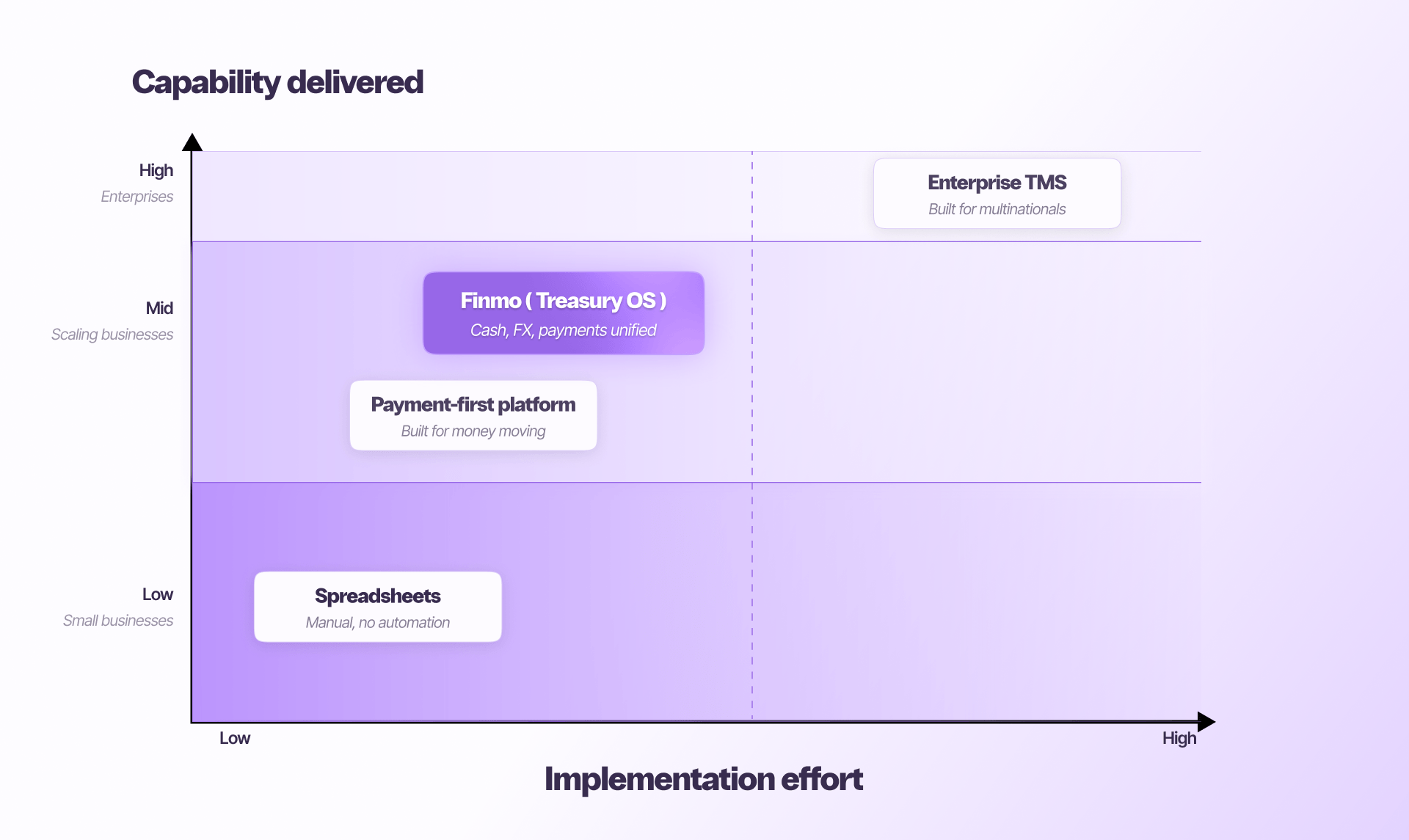

How the category compares: where a Treasury OS sits in the landscape

The treasury technology landscape has three distinct categories for finance teams to choose from. Each one sits at a different point on the trade-off between implementation effort and the depth of capability delivered.

Payment-first platforms sit in the low-effort, mid-capability range. They are easy to adopt, but limited to the cash that lives on the platform.

Enterprise TMS platforms sit at the opposite end of the scale, delivering deep capability but built for large multinationals with dedicated treasury teams. Implementation typically runs 12 to 18 months, with full functionality often taking longer, and selection requires engaging treasury specialists.

A Treasury Operating System like Finmo sits in the gap between them. It delivers the cash visibility, forecasting, FX management, and controls that finance teams need, without the implementation lift of an enterprise system. It is purpose-built for the middle, for finance teams that have outgrown payment rails but do not need a multinational-scale platform.

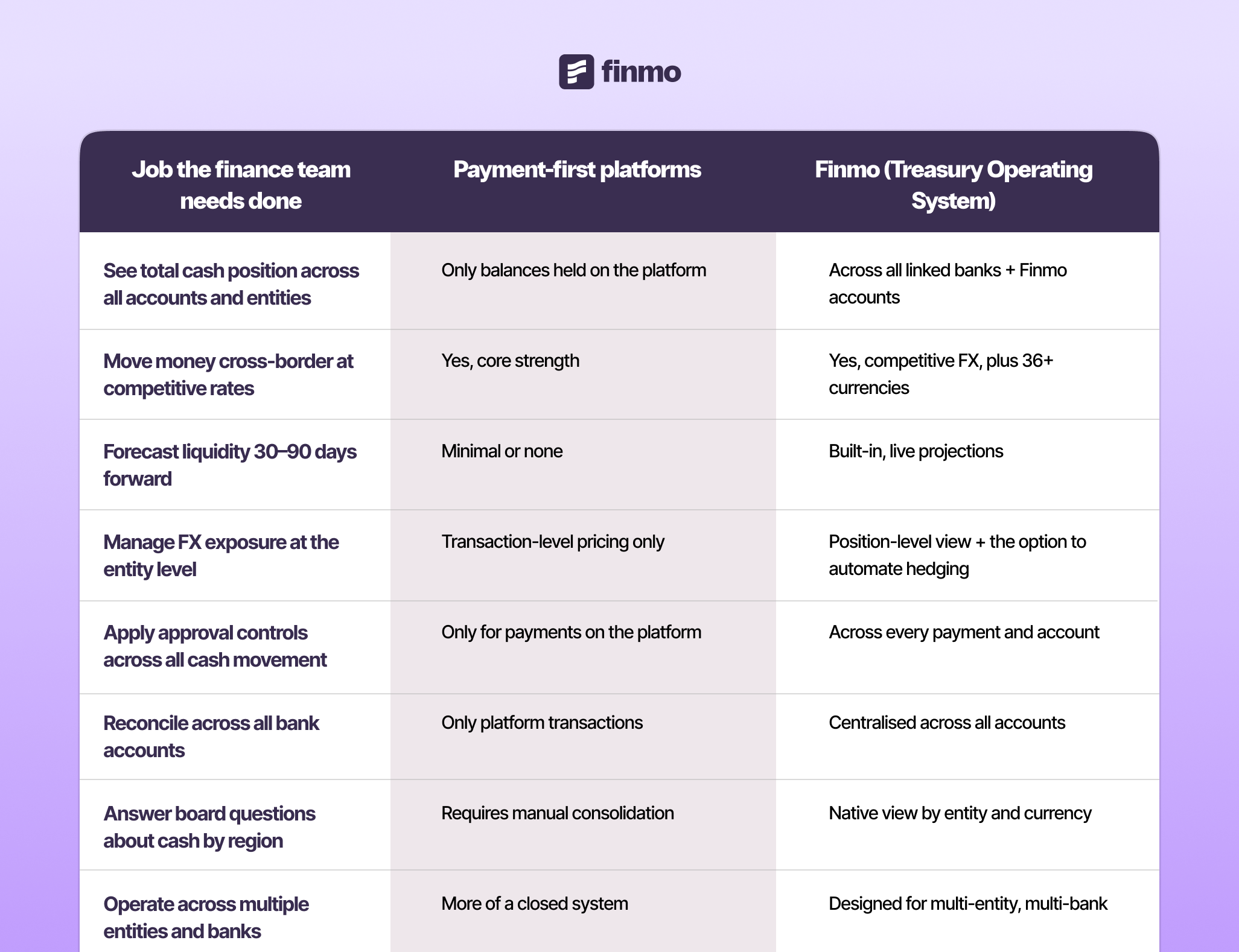

Side-by-side: Payment platforms vs Finmo (Treasury Operating System)

The cleanest way to compare the two categories is to look at the jobs a finance team needs done and ask which category is built to do them.

When to use a payment platform vs when you've outgrown it

Payment platforms work when

Your global business operates as a single entity, with one or two bank accounts, and your primary finance workflow includes sending or receiving international payments. Cash position is simple enough to check by logging into two tabs and reconciliation takes under an hour every month. You don't need real-time cash forecasts yet, and your board isn't asking for global cash positioning.

You need a Treasury OS when

You operate across three or more bank accounts, or multiple entities. Reconciliation currently takes hours every week when it should take seconds. You want to be able to produce forecasts that can to pull from live data, instead of week-old numbers. You also need support with approval workflows and FX risk management.

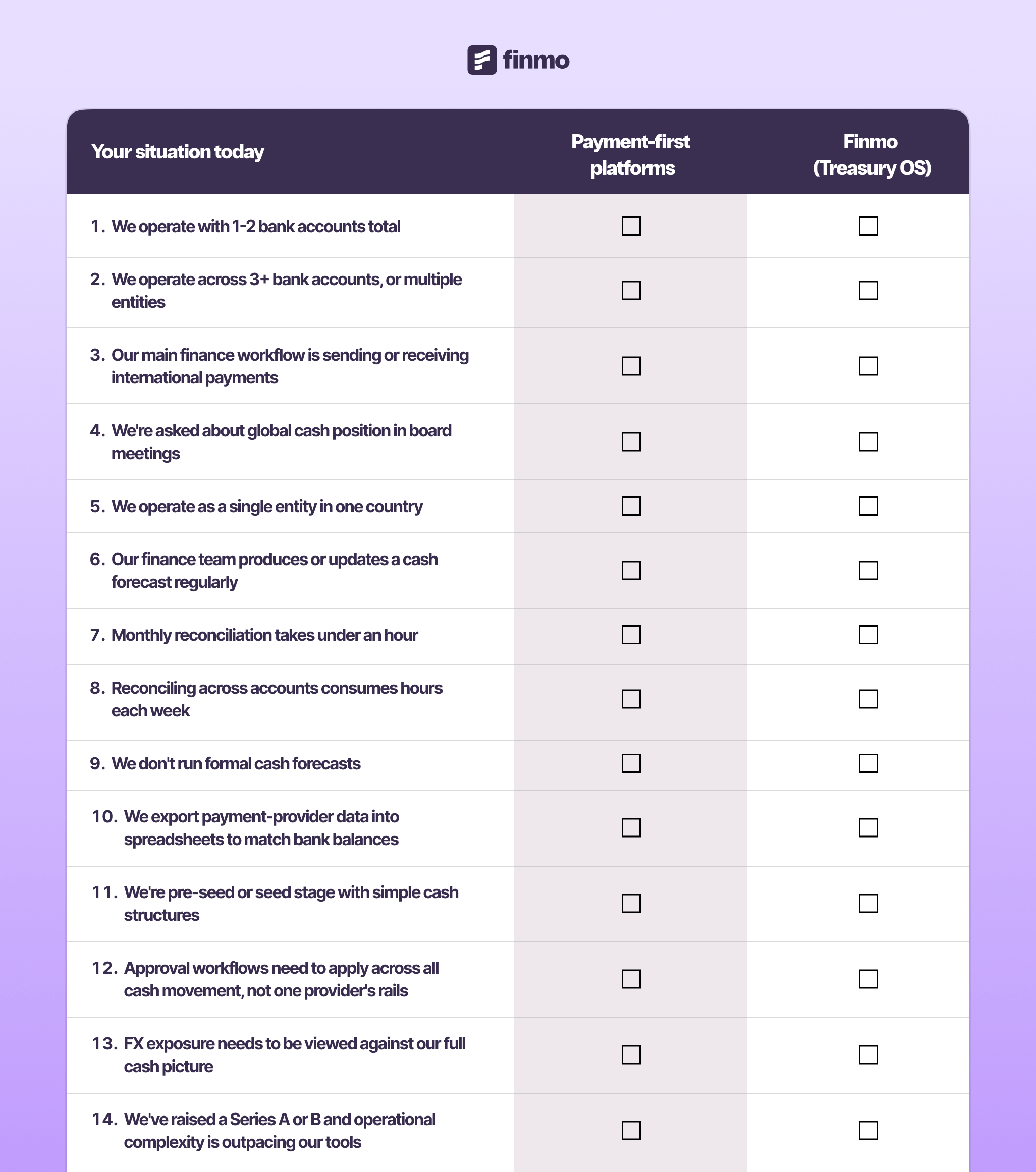

Self-diagnostic: Do you need Finmo or a payment-first platform?

Tick the boxes that match your current finance operations. Your count in each column points to the right category.

If most of your ticks land in the Finmo column, your job has shifted from moving money to managing a treasury function. A payment platform won't close the gap.

Why Finmo is more than just a payment provider

A payment platform is the right tool for moving money, but it was never built to manage a treasury function. As businesses scale globally, CFOs need a single source of truth to be able to answer questions about cash, exposure, and runway.

Finmo is built to be that source of truth. As a Treasury Operating System, it connects the bank accounts you already hold across every entity, opens multi-currency accounts in the markets you operate in, forecasts liquidity from live data, manages FX at the position level, and routes payments as one capability inside a broader operating layer.

If your finance team is exporting balances on Mondays to answer questions your board asks on Tuesdays, the tooling has fallen behind the business.

See how Finmo unifies cash and payments →

FAQ

What is a Treasury Operating System?

A Treasury Operating System (TOS) is software that manages a company’s complete treasury function–visibility across all bank accounts, liquidity forecasting, FX exposure, approval controls, and payments. It sits between payment-first platforms, which only focus on moving money, and enterprise treasury management systems, which are built for large enterprises with dedicated treasury teams.

How is a TOS different from a payment platform?

Payment platforms are built around cross-border transactions and hold cash inside a closed ecosystem. A TOS connects every account a company already holds, adds multi-currency accounts when needed, and treats payments as one capability inside a broader cash management layer.

Does Finmo replace my existing bank accounts?

No. Finmo connects the bank accounts you already hold across entities and currencies, so every balance is visible in one place. You can also open Finmo multi-currency accounts in 36+ currencies when you need them. Both sit in the same operating layer.